What is the National Pension System (NPS)?

The National Pension System (NPS) is a government-backed retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It allows individuals to invest regularly during their working years and receive a pension (annuity) after retirement. The money invested in NPS is managed by professional pension fund managers, and the returns are market-linked, making it one of the most efficient and transparent retirement planning tools.

NPS is open to:

All Indian citizens (Resident/Non-Resident) aged 18 to 70 years

Employees from government, corporate, and private sectors

Self-employed professionals and business owners

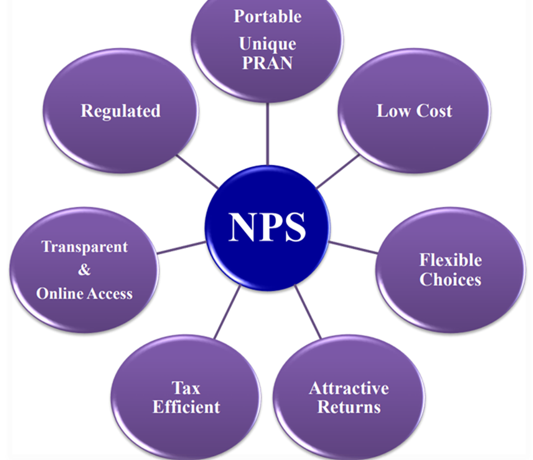

NPS is one of the best retirement planning tools offering a blend of security + market-linked growth + tax savings. With low costs, flexibility, and lifelong pension benefits, it is ideal for individuals who want a secured and stress-free retirement.

Page 2: Types of NPS Accounts, Investment Options & Tax Benefits

- Types of NPS Accounts

Feature | Tier I Account (Mandatory) | Tier II Account (Optional) |

Purpose | Retirement Savings | Voluntary Savings (like mutual funds) |

Withdrawal | Restricted till age 60 | Can withdraw anytime |

Minimum Contribution | ₹500 at opening | ₹1,000 to open |

Tax Benefits | Yes | No (except for Govt. employees) |

Lock-in Period | Till age 60 | No lock-in |

- Types of NPS Investment Choices

- Active Choice (You Decide Allocation)

You choose how your money is invested in:

- E – Equity (Max 75%)

- C – Corporate Bonds

- G – Government Securities

- A – Alternative Assets (Max 5%)

- Auto Choice (Life-Cycle Based Allocation)

Suitable for those who don’t want to manage investments. Allocation changes with age:

- Aggressive (LC75) – Higher equity till age 35

- Moderate (LC50) – Balanced equity & debt

- Conservative (LC25) – Lower equity, higher debt